15.12.2024

Financial struggles after marriage: A reader's plea for solutions to overcome deficit

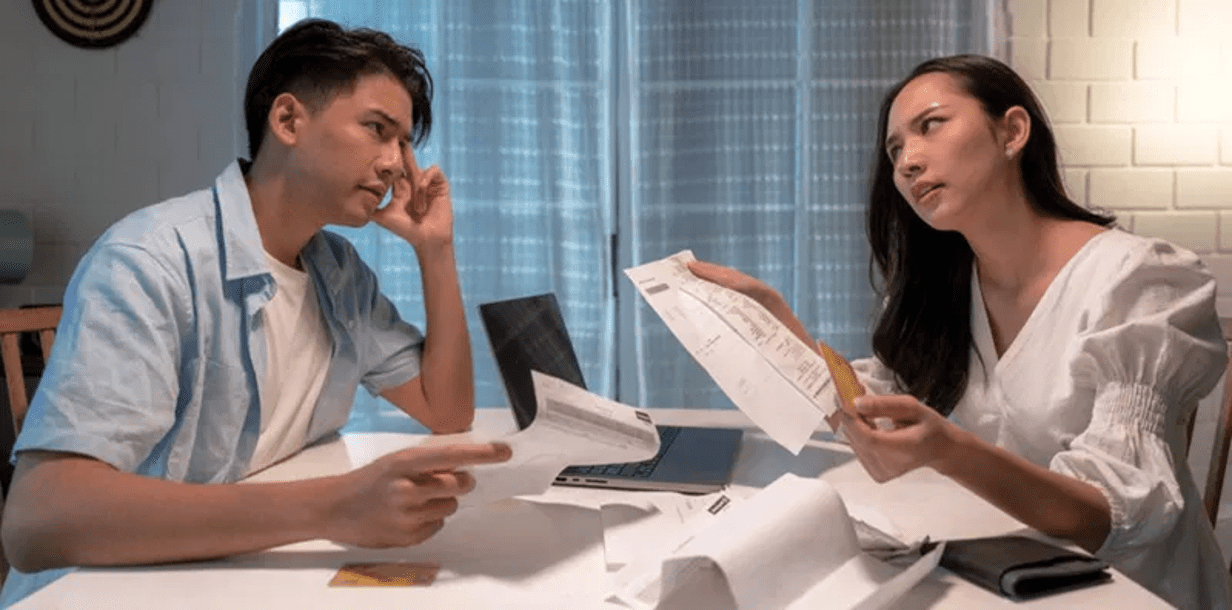

A 28-year-old reader seeks advice on managing financial strain after marriage, balancing family commitments, and tackling a monthly deficit. Is there a way to fast-track income and save his future?

.png)